In today’s rush society, we are becoming used to last minute, with many services suggesting that a ‘last minute deal’ would actually be better for our bank balance. However, this is not necessarily the case when it comes to investments.

Undoubtedly, the new financial year is not as exciting as a new calendar year. There’s no partying and no bonus days off work. However, there is a reason to celebrate. Being an ISA early bird could help you maximise any investment, all thanks to one critical component – time.

By investing early in the tax year, your investment can make the most of the time it has to grow. Admittedly, we don’t all have £20,000 ready and waiting to invest in one lump sum. This doesn’t however put you on the back foot. Drip-feeding into an ISA with a regular saving every month could actually generate a better return than investing a lump sum last minute.

A small sum, given years to grow, could do so much more than a larger sum invested at a later date.

By splitting an ISA allowance over a year, an investment could benefit, thanks to the magic that is *compounding. This regular investing can create a steady asset price, which in turn, can help maximise long-term returns.

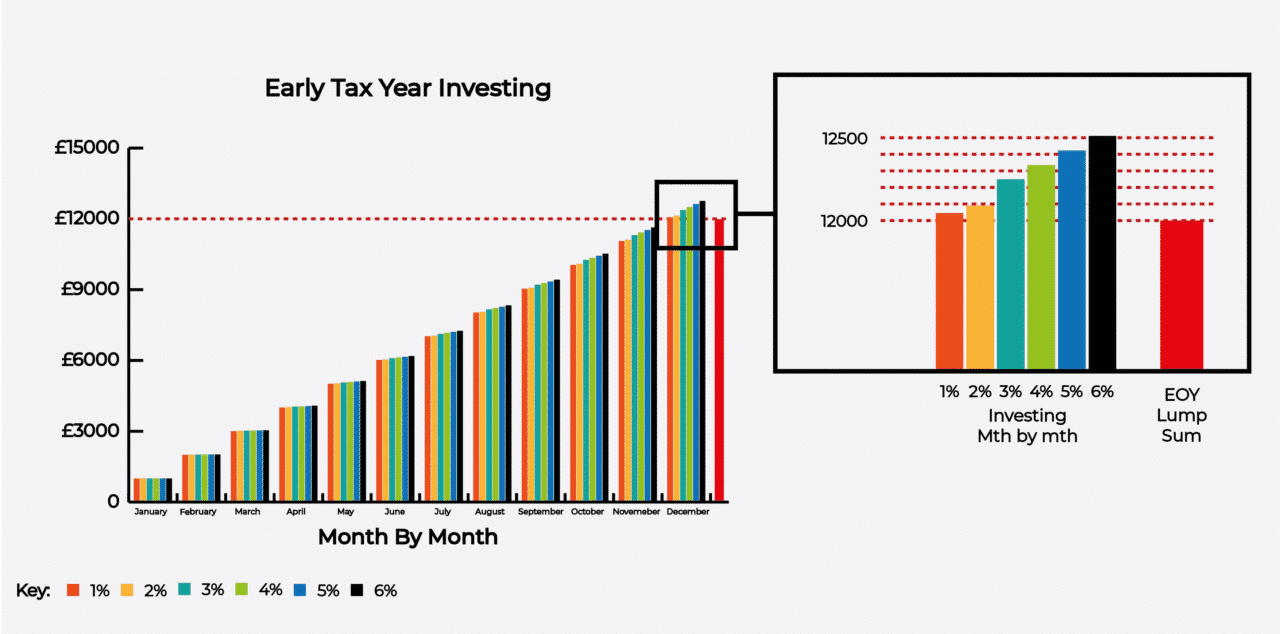

The below graph demonstrates the growth difference between a £12,000 lump sum investment and £1,000 a month.

By investing regularly over the long term, your returns could become substantial.

Additionally, monthly contributions also set you in good stead for an efficient saving habit and help you aim for your long-term goals.

So, wake up early and catch that worm, there’s no beneficial ‘last minute deal’ when it comes to investing.

*The maths around this can be a little muddling, but if you’re interested it’s a good idea to have a look at what the numbers could be.

{kind=link}